)%20(12).png)

Building Financial Literacy: 13 Key Personal Finance Terms

- Jun 27, 2024

- 5 min read

Updated: Jul 22, 2024

Writings and discussions on personal finance are often riddled with jargon that can overwhelm where they should provide clarity. Understanding a set of key terms on the subject can support your financial literacy and increase confidence when speaking with others about money (a practice I greatly encourage- let's normalize talking about money!) . Let's cut through some of the noise out there and breakdown 13 key finance terms that everyone should know.

General

Budget Ah. Everyone's favorite B-word... but, in all seriousness, the word budget does not have to be as intimidating as it is often made out to be. A budget is simply a written tracker of your desired cash flow, or how you want your money to come in and go out each month (or year). I like a particular quote that I heard in a training a long time ago, that "we all have a budget already, whether we acknowledge it or not." This is the key, I think. That the focus here is not judgment or shame about our actions, but rather, understanding what is already happening with our money, and being more intentional about our cash flow moving forward.

Emergency Fund A.k.a. “life happens” insurance. In the form of cash kept aside in case of emergency. When building your budget with purpose, we want to maximize your savings capacity while making sure that you aren't over-extending yourself financially. This includes making sure that you’re in a position to handle the unexpected. A healthy emergency fund is critical to any financial plan.

Retirement

401(k) A tax-advantaged retirement savings account offered by an employer as part of your employee benefits package (and compensation, when there is a match). For 2024, the maximum employee contribution to a 401k is $23,000. Similar employer-sponsored accounts that have the same contribution limit include 403(b)s and 457(b)s.

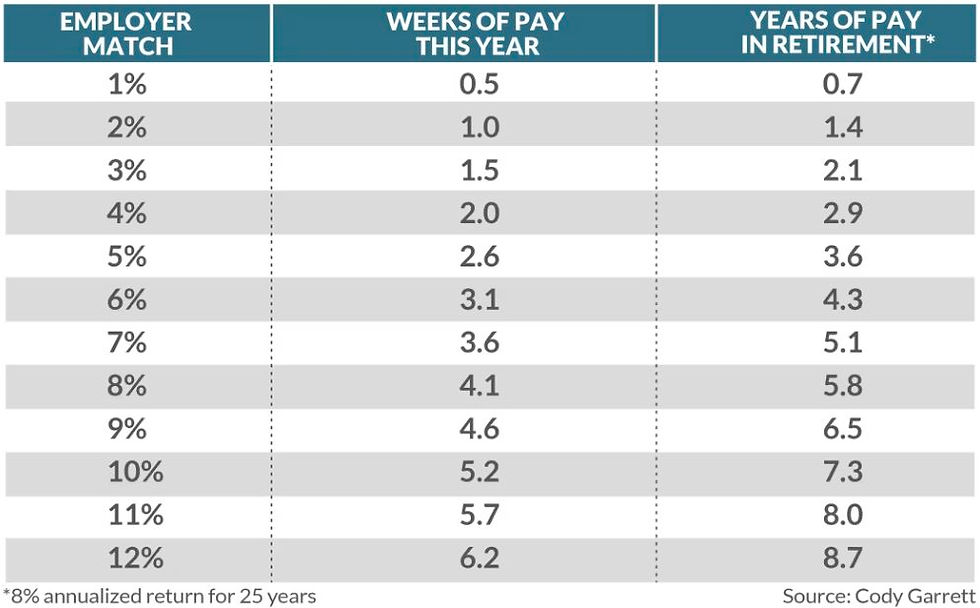

Employer Match When your employer matches a certain contribution amount to your employer-sponsored retirement account. It is usually a percentage but can be a flat dollar amount. Matches are a common offering yet are an oft-overlooked part of your total compensation package. They can be incredibly impactful to shorten your timeline to retirement, and are almost always worth taking advantage of.

Individual Retirement Account (IRA) A tax-advantaged retirement savings account opened and maintained by an individual, hence its name. Note: there are a couple of exceptions to the individual-only rule for self-employed workers. For 2024, the maximum IRA contribution is $7,000. This max is combined for both Traditional and Roth IRAs.

A note-

I hear confusion over 401ks and IRAs a lot. Both 401ks and IRAs are tax-advantaged retirement savings accounts. Other than that, they are fairly different.

Three main differences are:

Who offers them. An employer (401k) vs the individual (IRA).

Who is eligible to contribute to one. For example, IRAs have income limits to make regular contributions, while 401(k)s do not.

Their maximum contribution limits. As noted above, the contribution limits for these two accounts are very different. Both limits are set by the IRS and are reviewed annually to account for inflation.

Traditional Retirement Account (pre tax) You will pay taxes on all withdrawals from a traditional 401(k) or IRA in retirement. These accounts are great in that they offer a tax break at contribution *and* the invested funds grow tax deferred over the years, effectively delaying all taxation until retirement.

Roth Retirement Account (post tax) On the other side of the coin, contributions to Roth 401(k)s or IRA are post tax and thus do not save you anything on taxes today. They do, however, grow tax free, and all qualified withdrawals in retirement are tax free. If you are far out from retirement, Roth contributions can be a very powerful tool.

Investing

Asset Allocation Investing across various mediums, including stocks, bonds, real estate and cash. The right allocation for an investor depends on factors such as time horizon, risk tolerance and capacity (more on these below), flexibility and values.

Risk Tolerance The level of risk an investor is willing to take. Your risk tolerance relates to how you feel about risk.

Risk Capacity The level of risk an investment portfolio can take on. Your risk capacity is an objective assessment of the level of risk your portfolio should accept in order to efficiently reach your goals.

Passive Investing is typically a low cost, low maintenance, and globally diversified approach. This methodology isn't focused on picking individual stocks and bonds to invest in, but rather targeting different markets and asset classes to help diversify your overall portfolio. The idea here is that by investing in the majority of the global economy across a wide variety of funds, your portfolio will have diversification to help decrease your portfolio’s overall volatility while still efficiently balancing risk and expected return in support of your goals and investment needs.

Goal Planning

Pay Yourself First Paying your goals first and allowing discretionary spending second. The idea here is that each payday you transfer your goal money to a savings or investment account as determined by your financial plan. With this method, you pay towards your goals first and then allow yourself to spend whatever is left in your checking account after your fixed bills on discretionary expenses.

FI (Financial Independence) Number This (very fun) number is the estimated amount you would need to retire, say, tomorrow. It is also called the 4% rule. Based loosely on the Trinity study originating in the 90s, essentially, research of investment withdrawals over time show a likelihood that an investor could withdraw a certain amount annually for 30+ years and not run out of money. The actual percentage the FI community likes to use varies from about 3-5% of total portfolio balance, depending on one's risk tolerance. In short, you can calculate your FI number by adding up your annual expenses and multiplying it by:

33.33 for the more conservative 3% rule

25 for the more popular 4% rule

20 for the more flexible 5% rule

The number you come up with is your FI number. There are lots of factors that affect retirement need and distributions, but this is an exciting starting place to have in mind as you save up for retirement, and hopefully, financial freedom even earlier.

Alright, we'll stop there for today with the terminology. We hope that you learned a new term or two from this article, maybe found clarity on another, and that you are that much more prepared and confident to talk all things money at your next dinner conversation.

• • •

Drop a comment on this post to let us know a financial term you'd like to see included here.

Need help putting together your financial plan? Get in touch.

#financialplanning #money #moneymindset #goals #success #personalfinance #millennials #genz #womenandmoney #financialwellness #financialfreedom #CFP #FinancialPlanningMonth #moneysaver #moneymanagement #financetips #moneygoals #financialliteracy #financialeducation #financialindependence #FI #FIRE #moneymoves #womenempowerment #womeninbiz

📌 Sage Financial Planning LLC helps first generation wealth builders know, feel and do better with their finances to help them achieve their life goals and, eventually, reach financial freedom.

For more information on our holistic financial planning offerings, please visit our Service Options page.